Exchange Scenarios in Tacoma, Washington

Want to Make Your 1031 Exchange Successful?

Call Today to Speak with a Real Estate Attorney

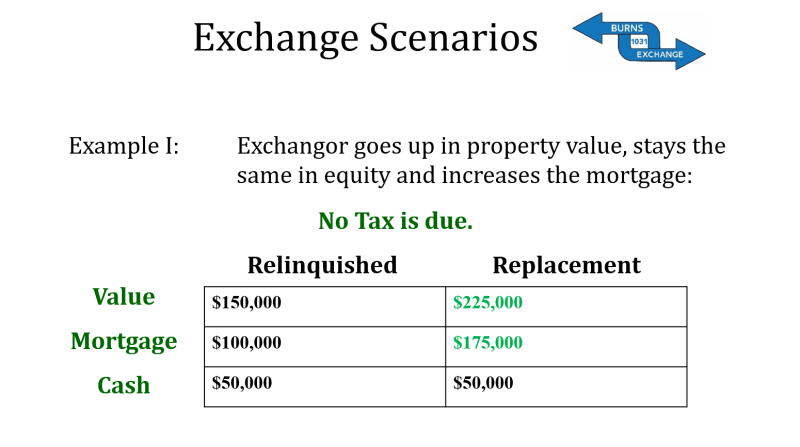

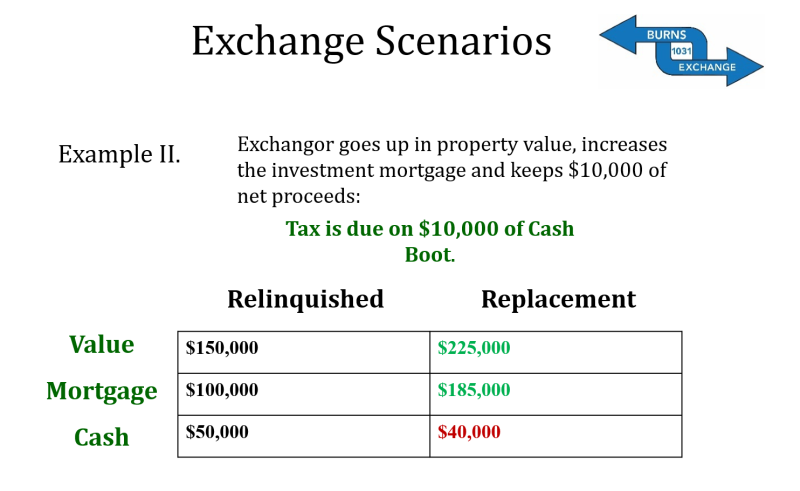

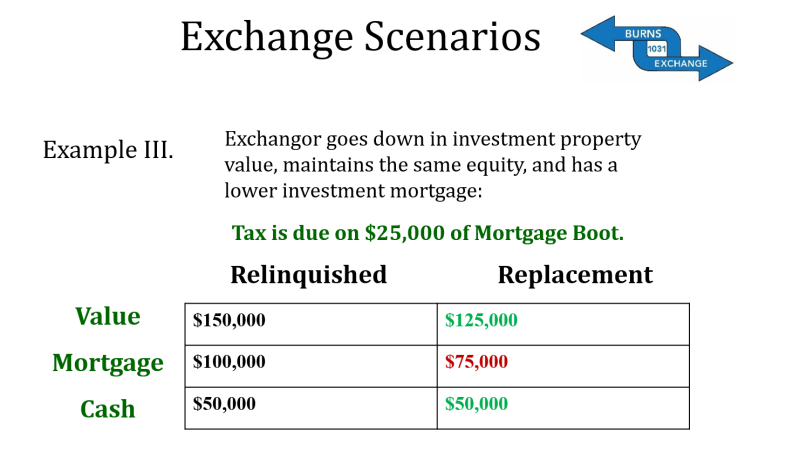

In order to obtain a deferral of the entire capital gains tax, the Exchangor must:

Purchase replacement property of equal or greater value to the relinquished property. Failure to do so will result in a partial exchange, and some tax will be due.

Reinvest all of the net proceeds from the relinquished property in the replacement property.

Obtain equal or greater financing on the replacement property than was paid off on the relinquished property.

Receive nothing in the exchange but like-kind property.

To the extent the Exchangor fails to observe these rules, they will be subject to capital gains tax.

Time Limits

There are important, hard-and-fast time limits related to the completion of a successful 1031 Tax Deferred Exchange.

45-Day Rule: The Exchangor must identify the potential property or properties within the first 45 days after the relinquished property sale closes. This identification must occur in writing.

180-Day Rule: The Exchangor must acquire the replacement property or properties within 180 of the closing on the relinquished property or the date the Exchangor must file a tax return (including extensions) for the year of the transfer of the relinquished property, whichever comes first.

There are no extensions of either the 45-Day Rule or the 180-Day Rule for Saturdays, Sundays or holidays.

The time limits begin to run on the date the Exchangor transfers the relinquished property to the buyer.